Expert Insights Powered by Ramez Dandan: Former CTO, Microsoft Middle East | 30+ years in IT & Telecom.

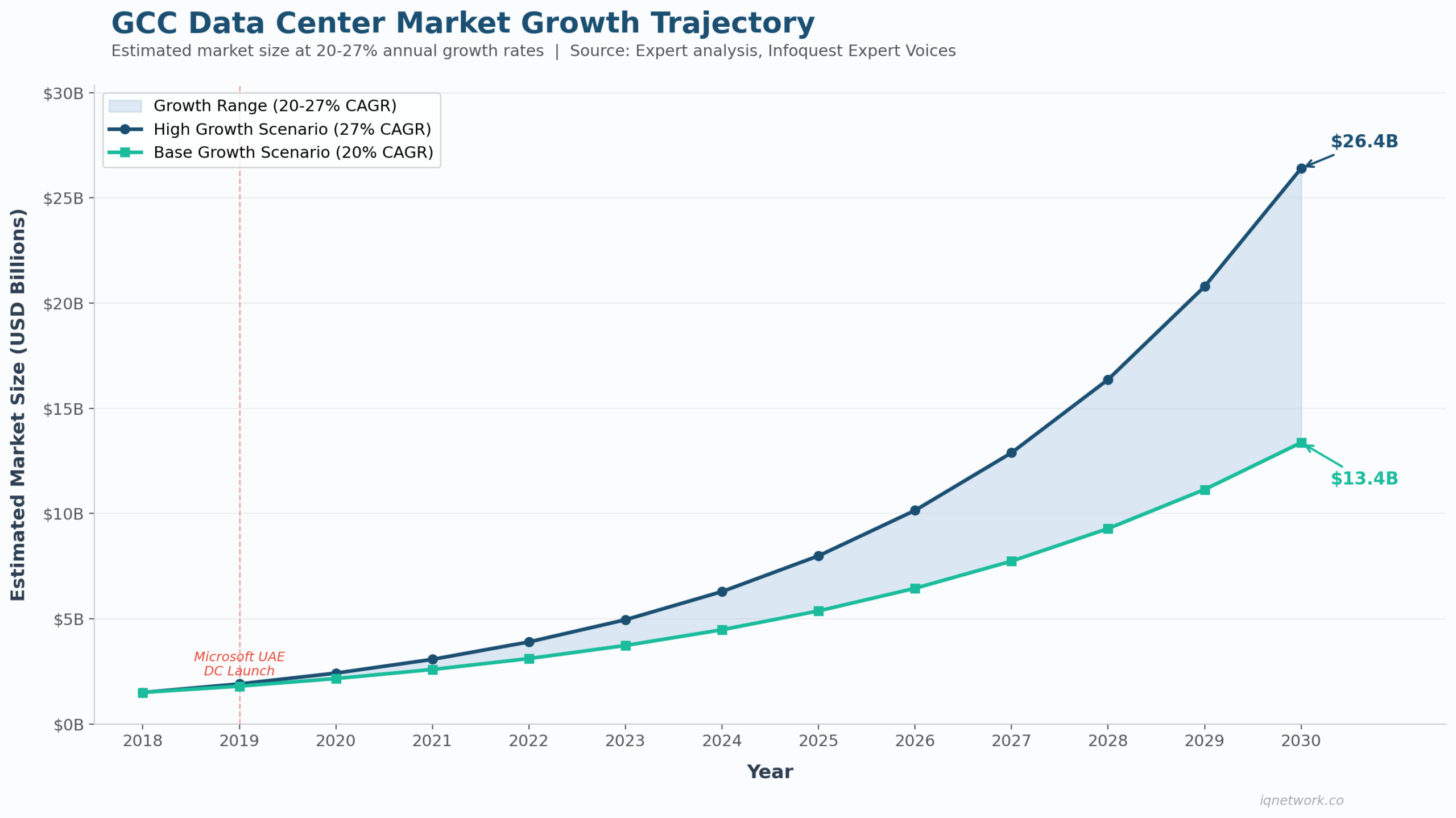

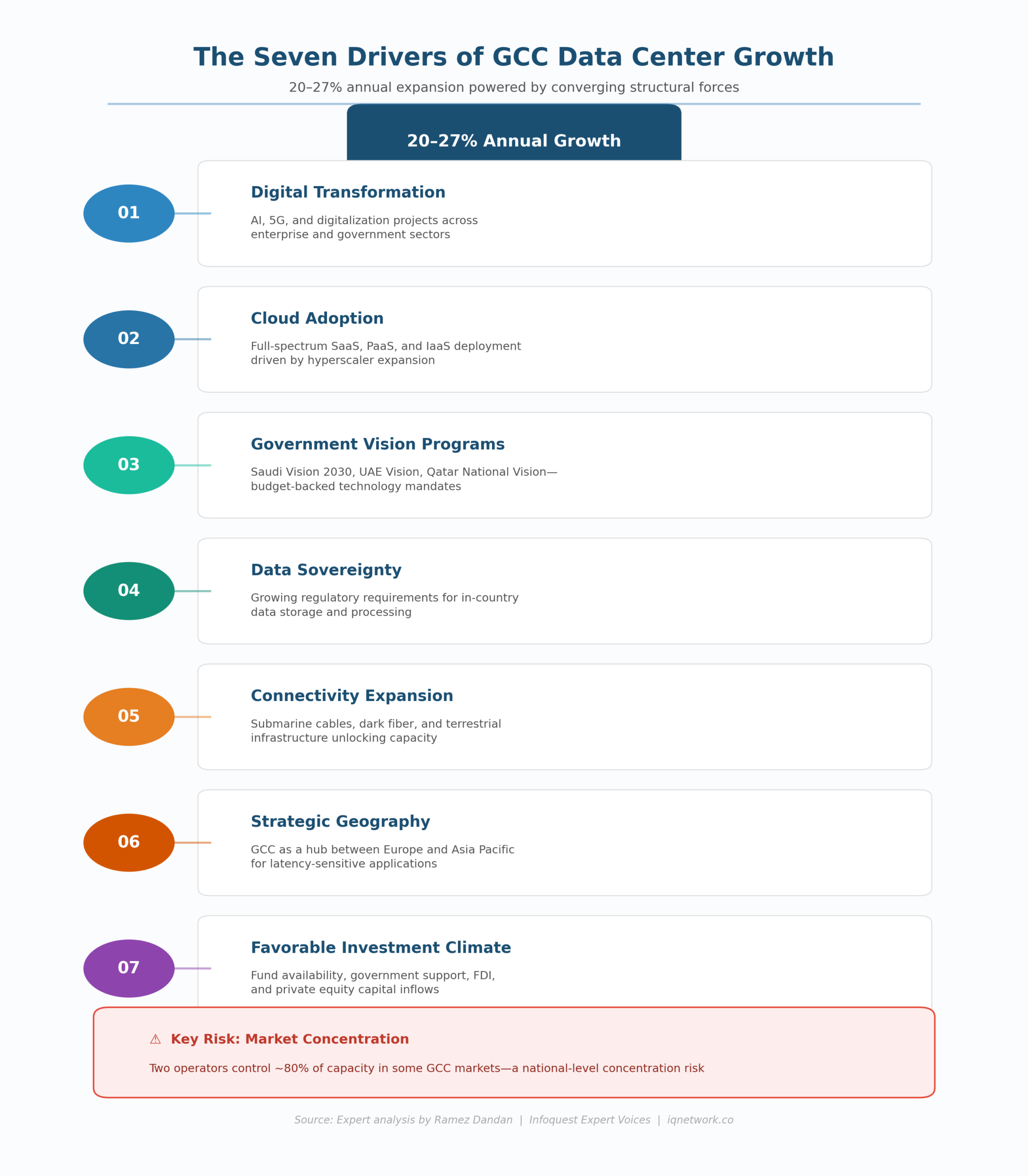

The GCC region has emerged as one of the fastest-growing data center markets globally, with annual expansion rates estimated between 20 and 27 percent. While this growth rate commands attention from investors and operators worldwide, the underlying dynamics driving this expansion are often oversimplified or misunderstood. Moreover, the GCC data center growth story is not a single narrative—it is the convergence of at least seven distinct forces. Each of these forces reinforces the others.

To unpack the GCC data center growth, Infoquest spoke with Ramez Dandan, a technology strategist with over 30 years of experience across IT and telecommunications in the Middle East. During his tenure as CTO at Microsoft, Dandan led the establishment of Microsoft’s first regional data center in the Middle East. This was a three-year initiative that launched in 2019. It provided him with direct, operational insight into both the promise and the friction of building critical digital infrastructure in the region.

“We’re still on the maturity curve, but we’re moving fast.”

Driver 1: Digital Transformation as the Demand Foundation

The most fundamental driver of data center demand in the GCC is the acceleration of digital transformation across both enterprise and government sectors. Projects leveraging AI, 5G, and broader digitalization initiatives are creating sustained demand for compute and storage capacity.

“The projects that companies and governments are pushing forward utilizing technologies like AI, 5G, and digitalization in general, that’s a key driver of demand for data centers.”

This is not abstract. Government-led smart city programs, enterprise cloud migrations, and the rollout of 5G networks across the UAE, Saudi Arabia, and Qatar are all generating tangible, recurring demand for data center capacity. According to Mordor Intelligence, the Middle East and Africa region’s cloud market is expected to reach $14 billion by 2030. Notably, the GCC accounts for the majority of that growth.

Driver 2: Cloud Adoption Across All Service Models

Cloud adoption in the GCC has moved well beyond early experimentation. Organizations are now deploying across the full spectrum of cloud service models—software as a service, platform as a service, and infrastructure as a service. Consequently, this is driving significant demand for hyperscale data center capacity.

“Cloud adoption with all its flavors, software as a service, platform as a service, infrastructure as a service, all things that you can do more and more applications. The cloud adoption is driving demand for data centers, and that’s primarily driven by the large hyperscalers.”

The entry of major hyperscalers such as Microsoft Azure, Amazon Web Services, Google Cloud Platform, Oracle, and Alibaba Cloud into the GCC has been a catalytic force. These operators are not merely renting space; additionally, they are shaping facility design standards, operational benchmarks, and ecosystem expectations across the region.

Driver 3: Government Vision Programs

Multi-year national transformation agendas such as Saudi Vision 2030, UAE Vision, Qatar National Vision, and Dubai’s D33 strategy explicitly emphasize technology adoption as a lever for economic diversification, employment generation, and global competitiveness. These are not aspirational white papers; further, they carry budget allocations and regulatory mandates that directly translate into data center demand.

“Saudi Vision 2030, Abu Dhabi Vision, UAE Vision, Qatar, Dubai Vision, these initiatives emphasize the use of technology and the leverage of technology to develop economic diversity and growth and employment.”

Driver 4: Data Sovereignty Requirements

An increasingly important driver is the growing appetite across the GCC for sovereign control over data. Regulatory frameworks in the UAE, Saudi Arabia, and Bahrain now include data localization requirements for specific sectors, particularly government, financial services, and healthcare. This is accelerating investment in in-country data center capacity. It reduces reliance on facilities in Europe or Asia.

Driver 5: Connectivity Expansion

Dandan describes connectivity as “the blood” of the data center ecosystem. Expanded submarine cable landings, dark fiber networks, and terrestrial connectivity upgrades are unlocking capacity. Previously, this was constrained by infrastructure limitations.

“Connectivity is the blood; if it’s constrained, then the body is not going to grow. More connectivity drives more data center investments.”

Driver 6: Strategic Geographic Positioning

The GCC sits at the crossroads between Europe and Asia Pacific, two of the world’s most heavily resourced data center markets. This geographic position makes the region a natural hub for latency-sensitive applications, gaming, communications platforms, and content delivery networks. Dandan notes that this positioning is increasingly understood at the government level. Furthermore, it is now actively being leveraged to attract international digital infrastructure investment.

Driver 7: Favorable Investment Environment

The final driver is the overall investment climate. Fund availability, government co-investment programs, streamlined ownership structures, and efficient construction permitting create a favorable environment for large-scale data center development. What was once primarily supported by large regional enterprises and telcos has now attracted significant foreign direct investment. In addition, private equity capital is pouring in.

“Initially, it was supported by big enterprises in the region, telcos, then governments, then semi-government, and now we’re seeing a lot of private equity come into this space from outside.”

The Risks Beneath the Growth Story

Despite the compelling growth trajectory, Dandan identifies several structural risks that warrant attention. The most significant is market concentration: in some GCC countries, as few as 2 operators control apx. 80 % of data center capacity.

“You’re talking about 80% of the market covered by two players; that’s a concentration risk. If you have a problem and 40% of the capacity goes out, you have a national disaster.”

Additional challenges include persistent gaps in cost parity relative to more mature markets, ongoing skilled labor shortages, regulatory frameworks that lag behind technology adoption, and connectivity infrastructure that, while improving, remains insufficient for the region’s ambitions. Dandan characterizes these as addressable gaps rather than fundamental barriers. Also, he notes they are actively being worked on across the region.

Strategic Implications

For investors, the GCC data center market offers a rare combination of high growth rates and structural tailwinds. However, successful deployment requires understanding the nuances of each market—the regulations, power availability/cost, and connectivity differ between GCC countries.

For operators, Dandan’s advice centers on customer proximity and strategic partnerships. In a market where concentration risk is real, diversification is not merely good practice. Instead, it is an industry imperative.

“Approaching customers as partners and not just tenants is key. It’s a win-win.”

About the Expert

Ramez Dandan is a technology strategist with over 30 years of experience in IT and telecommunications across the Middle East. He served as Chief Technology Officer at Microsoft for the last seven years of his 17-year tenure, where he led the establishment of Microsoft’s first regional data center in the Middle East. His expertise spans digital transformation, cloud infrastructure, and technology policy advisory for enterprise and government clients across the GCC.

Access Expert Insights Through Infoquest

This article is based on an expert consultation conducted through the Infoquest expert network. Organizations seeking deeper analysis of GCC data center infrastructure, investment due diligence, or direct access to experts like Ramez Dandan can reach out to us below.

Need Expert Insights?

Connect with Ramez or similar expertsThis article is also supported by data from: